By

Joel Robinson

•

2

min read

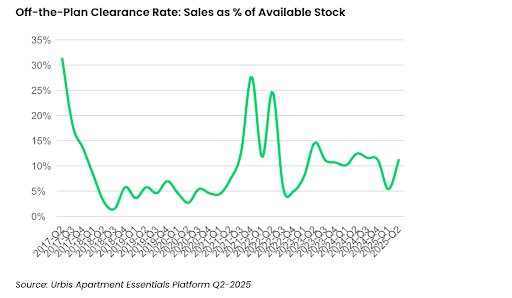

The key demand-versus-supply metric in Sydney’s off-the-plan apartment market is skewing toward higher demand, according to the latest Urbis Apartment Essentials report.

The quarterly report analyses off the plan sales, new apartment rents, and the supply of BTS and BTR product across Australia. It showed a notable uptick in clearance rates for off-the-plan apartments over Q2 2025.

Urbis found that sales as a proportion of available stock lifted from five per cent in Q1 to 11 per cent in Q2. Urbis Director Alex Stuart attributes this to growth in the high-end apartment market and continued sales in staged developments.

"We are seeing strong launches in new projects followed by periods of more stable sales, as affluent buyers are generally more discerning in their purchases," Stuart said.

Purchases are still majority driven by owner-occupiers, who accounted for around 70 per cent of sales in Q2 2025. Stuart says that while this has been the case for several quarters, lower interest rates and positive sentiment are likely to draw investors back into the market, though not to the levels seen in the pre-COVID era.

In 2019, investors accounted for well over 60 per cent of Sydney off the plan transactions, with around a quarter of purchases from foreign investors. That demand has since been stifled nationally after governments lifted stamp duty surcharges for foreign purchasers from four per cent to eight per cent, and steadily increased land tax surcharges from 0.75 per cent to five per cent in 2025.

While the federal government recently introduced a temporary two-year ban on foreign buyers purchasing existing homes (from April 1, 2025), anecdotal feedback suggests this hasn’t pushed foreign purchasers into the off the plan market yet, due to the higher duties and Foreign Investment Review Board (FIRB) application fees.

.png)

Meanwhile, Sydney continues to face a major undersupply of apartments. The NSW Government has set ambitious housing targets, but current forecasts fall well short. Urbis completion data highlights how deeply the pandemic disrupted construction, with 2025 likely to deliver completions on par with 2020. Looking ahead, completions expected in 2026 could dip back to just over 6,000 apartments, almost half the level expected in 2025.

"Apartment completions in the Sydney Essentials Region are estimated to average 9,200 per year in 2025 and 2026," Stuart says. "This is well below the average completions of 14,700 per year in the pre-COVID period of 2016–2019. This highlights the continued undersupply of the Sydney housing market."

.png)

A lack of new project launches is also feeding the undersupply, with many developers exiting the market or delaying starts until conditions improve. There were just 34 project launches in the Sydney Essentials Region in FY25. While that reflects some stabilisation following a steep decline, it is still well below the 70–100 launches per year recorded between FY19 and FY22.

Most of the recent launches have been concentrated in Sydney’s inner areas and the Lower North Shore, highlighting that only premium locations are currently able to justify the higher prices needed to make projects viable in today’s elevated construction cost environment.

.png)

Stuart says the market is in a positive upswing with falling interest rates increasing buyer confidence, which is anticipated to drive off the plan demand. The macroeconomic environment and supply shortfall is also anticipated to drive price growth in the second half of 2025. In the short term, developer activity is anticipated to continue to be focussed on Inner Ring locations with developers historically more active in suburban locations expanding to more premium locations.

Speak to the team about leveraging the Apartments.com.au audiences and services for your new development.

Greg Billings

Director of Residential Projects

Sonia Fava

Director

Nick Clydsdale

Senior Director

Heath Thompson

Director

Todd Matheson

Director

Thomas Panson

Project Sales & Marketing Agent

Scott Jessop

Head of Sales & Marketing

Alex Adams

Head of Sales & Marketing and

Head of New Business

.jpeg)

.png)

-03.png)

.png)

.png)

.png)

_page-0001.jpg)

.png)

.png)

.png)

-01.png)

%20(2)-01.png)