By

Michael Bird

•

30

min read

South East Queensland remains one of the most active apartment markets in the country, but the development conversation has shifted. Demand is not the problem. Feasibility is.

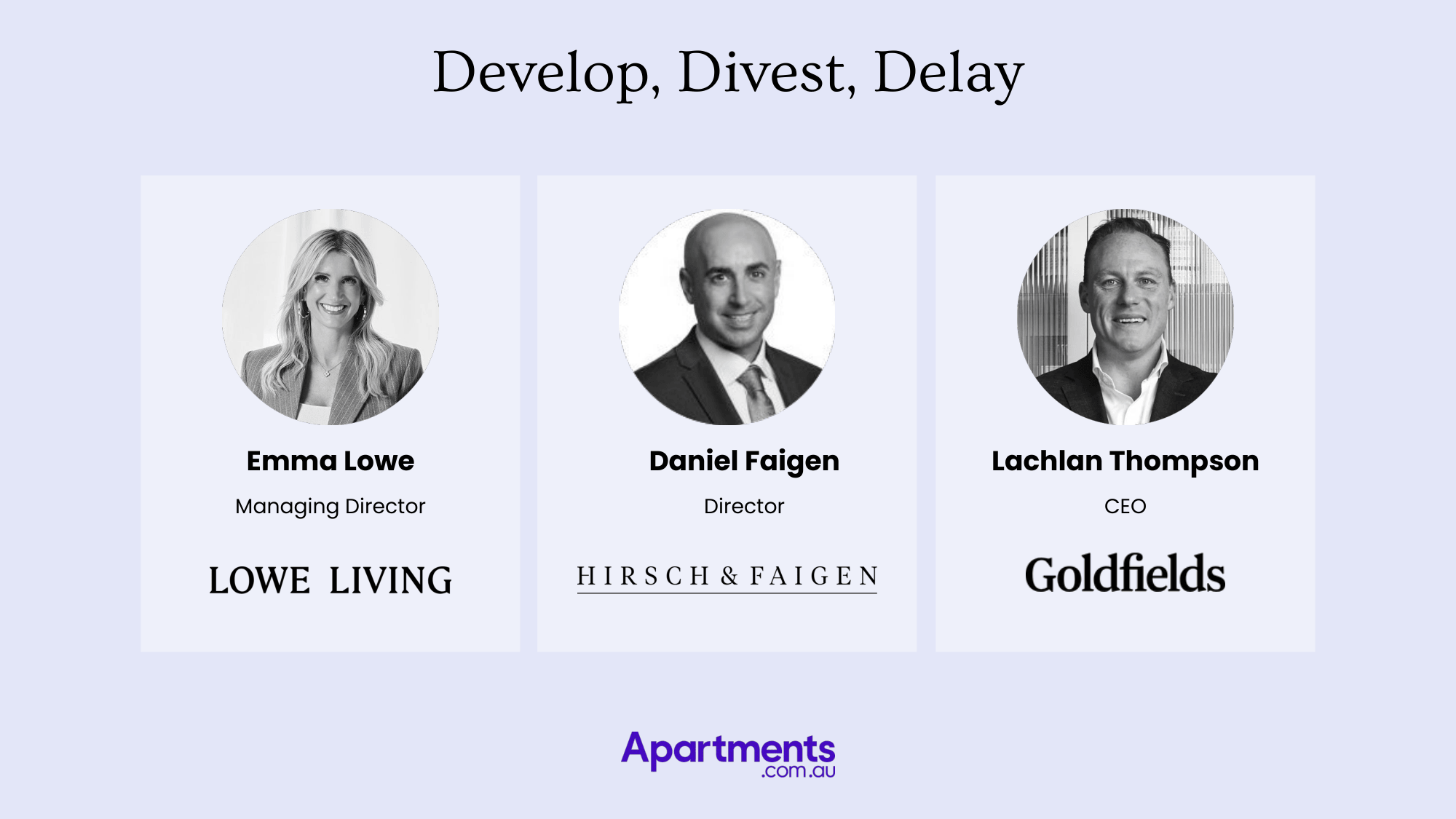

In this live panel 'Developing South East Queensland' panel, Mike Bird, CEO of Apartments.com.au, is joined by Christie Leet (Sherpa), John Kearney (Immerse Projects), David Stone (Centuria Bass) and Sam Gardner (Gardner Vaughan Group) to unpack what is really driving site decisions across the Gold Coast, Brisbane and the broader SEQ pipeline.

The session moves beyond general market commentary and into the decisions that matter most right now: which sites get developed, which get divested, and which get delayed until the numbers work again.

The panel’s central theme is clear. There is still significant opportunity in SEQ, but not every well located site is viable in today’s cost environment. Developers are becoming more selective, and the gap between “good” and “buildable” is widening.

Across the discussion, four practical filters emerge as the deciding factors for site acquisitions and launch decisions.

Sam Gardner shares a blunt benchmark from within Gardner Vaughan Group’s delivery pipeline. Construction costs have increased dramatically over the past several years. While the rate of increase has started to soften, the panel does not expect a meaningful fall in absolute costs.

The discussion points to a shift in tender dynamics. Builders are seeing more competition than they did during the peak period, with more trade participation across packages. That competition may help reduce escalation pressure, but it does not reverse the new base cost of delivery.

The takeaway for developers and project teams is straightforward. Feasibility now depends less on hoping costs will fall, and more on designing a project that builds cleanly, sells clearly, and carries minimal complexity.

If there was one metric repeated with real urgency, it was efficiency.

Christie Leet frames building efficiency as underappreciated and often misunderstood, particularly when teams assess approved sites in isolation. A project can have a strong location and a valid approval and still fail feasibility because the built form does not convert enough gross building area into saleable area.

Christie highlights a common issue in the current market. Many approvals come with saleable efficiency in the 45 to 50 per cent range. Unless pricing is at the very top end of the market, these projects often cannot absorb current construction costs.

For Sherpa, this is why the search for sites has become more specific. The team looks for dimensions and planning settings that support efficient basements, efficient parking, and a consistent apartment yield that aligns with their model.

The message is relevant for developers, project marketers and consultants alike. The market is not just rewarding good locations. It is rewarding projects that are easy to deliver, easy to understand, and priced within clear buyer depth.

The panel also reframes how developers define an A grade site.

For Gardner Vaughan Group, A grade is not simply a prestige suburb or a headline location. It is proximity, measured by what a buyer can access within a short walk or short drive.

This emphasis reflects how buyers are behaving now. Amenity, transport links and lifestyle access remain core drivers of absorption, but they also provide a defensive advantage when pricing pressure rises. If a project sits in a pocket where the buyer can park the car and access everything in five to ten minutes, it is easier to justify the price point.

From a demand and marketing perspective, it is the difference between a project that sells on lifestyle and convenience and one that must sell purely on discount.

John Kearney makes a point that resonates with any developer who has stared at a feasibility spreadsheet for too long. There is no point buying a site if you do not have a delivery solution.

For builder developers and vertically integrated groups, that reality is even sharper. The first question is not what the approval says. It is whether the project matches the capability of the delivery team that will actually build it.

This “delivery first” approach is becoming more common in SEQ as trade availability, program certainty and builder performance play an outsized role in risk.

A standout feature of the session is a live site review, where the panel applies its frameworks to real examples across the Gold Coast corridor.

A large Surfers Paradise Boulevard opportunity highlights the difference between site appeal and project fit. Several panellists describe it as too large or too complex for their current model unless it could be staged, subdivided, or secured on exceptional vendor terms. The discussion also reflects a reality of premium coastal land. If the site becomes an international play, local developers may be competing against groups willing to pay cash and accept long holds.

A smaller approved scheme in Coolangatta shows the challenge of boutique projects that still require a high level of design and delivery effort. The panel suggests that a 34 apartment project can demand the same intensity as a much larger development, which changes the return profile. The consensus leans toward divest or delay unless revenue assumptions shift materially.

A beachfront full floor product demonstrates the upper end risk profile. Several panellists describe the market depth as narrower for multi million dollar full floor apartments, noting that sales can be discretionary and volatile if conditions tighten. This is where lender requirements such as higher pre sale coverage become more relevant.

Robina prompts a different conversation. Some panellists view it as a hold, driven by planning and policy settings that may evolve and unlock better outcomes over time. Others note that without the right scale or allocations, the site may not work today. The common thread is that Robina has fundamentals, but viability depends on planning certainty and the ability to unlock yield without delay.

David Stone outlines how private lenders assess SEQ opportunities, with a strong focus on sponsor capability and execution risk.

Centuria Bass supports developers seeking flexibility outside bank appetite, but remains cautious about extensive planning risk. The reasoning is commercial and simple. Time kills feasibility.

Without a proven ability to negotiate planning outcomes quickly and deliver a project to program, interest carry can erode equity rapidly, particularly where developers do not have secondary cash flow to service facilities during delays.

From a developer perspective, the takeaway is that capital is available, but the bar is higher. Balance sheet matters, delivery track record matters, and speed to commencement matters.

Across the conversation, the panel signals several practical shifts happening in SEQ.

South East Queensland still offers a deep runway of opportunity, but the market is now defined by constraints. The winners will be the groups who combine the right site selection with the right delivery solution and the right efficiency metrics.

Demand is there. Capital is there. The question is whether the project can be delivered without delay, priced within real buyer depth, and designed to convert as much of the building as possible into saleable outcomes.

That is the feasibility filter. And in this cycle, it is the deciding factor.

.jpeg)

Speak to the team about leveraging the Apartments.com.au audiences and services for your new development.

Greg Billings

Director of Residential Projects

Sonia Fava

Director

Nick Clydsdale

Senior Director

Heath Thompson

Director

Todd Matheson

Director

Thomas Panson

Project Sales & Marketing Agent

Scott Jessop

Head of Sales & Marketing

Alex Adams

Head of Sales & Marketing and

Head of New Business

.png)

-03.png)

.png)

.png)

.png)

_page-0001.jpg)

.png)

.png)

.png)

-01.png)

%20(2)-01.png)